Top Wealth Transfer Strategies to Protect Your Legacy

Protecting Your Family's Future: A Guide to Effective Wealth Transfer

Building and preserving wealth takes dedication; transferring it wisely takes strategy. This listicle outlines six key wealth transfer strategies—Irrevocable Trusts, Gifting Strategies, Family Limited Partnerships (FLPs), Charitable Remainder Trusts (CRTs), Grantor Retained Annuity Trusts (GRATs), and Qualified Personal Residence Trusts (QPRTs)—to secure your family's financial future. Learn how these wealth transfer strategies can minimize estate taxes, maintain family control over assets, and support philanthropic goals. We'll explore the advantages and disadvantages of each, offering practical examples to guide your decision-making. PARK Magazine's wealth management expertise will help you craft a legacy that reflects your values.

1. Irrevocable Trusts: A Powerful Wealth Transfer Strategy

Irrevocable trusts stand as a cornerstone in the realm of sophisticated wealth transfer strategies. They offer a robust mechanism for high-net-worth individuals to safeguard and distribute their assets while minimizing tax burdens and ensuring long-term financial security for future generations. This legal arrangement involves transferring assets from an individual's estate into a trust that, as the name suggests, cannot be easily modified, amended, or terminated without the consent of the designated beneficiaries. This transfer effectively removes the assets from the grantor's taxable estate, significantly reducing potential estate tax liability.

Once assets are placed within the irrevocable trust, the grantor relinquishes control over them. This is a crucial distinction from revocable trusts, where the grantor retains ownership and control. The irrevocable nature of these trusts offers distinct advantages for wealth preservation and tax mitigation, making them a prominent choice for high-net-worth individuals seeking comprehensive estate planning solutions. There are several types of irrevocable trusts, each designed for specific objectives: Irrevocable Life Insurance Trusts (ILITs) hold life insurance policies, removing death benefits from the estate; Charitable Remainder Trusts (CRTs) provide income for beneficiaries and ultimately benefit a designated charity; and Generation-Skipping Trusts (GSTs) facilitate the transfer of wealth to grandchildren or later generations, bypassing estate taxes at the children's level. Further, irrevocable trusts can be structured for specific purposes, such as funding education or providing for special needs care.

The benefits of utilizing an irrevocable trust are numerous. They provide substantial estate tax reduction, often a primary driver for their implementation. They also offer a layer of asset protection from creditors, shielding wealth from potential legal challenges. The controlled distribution of wealth across generations is another key advantage, allowing grantors to define how and when beneficiaries access assets. Moreover, trusts generally avoid probate, maintaining privacy and streamlining the wealth transfer process. Finally, spendthrift provisions can be incorporated to protect beneficiaries from their own potentially detrimental financial decisions.

However, irrevocable trusts are not without their drawbacks. The most significant is the loss of control over the assets once they are transferred. This irreversibility necessitates careful planning and consideration. Establishing and maintaining these trusts can be complex, requiring specialized legal and financial expertise, and therefore, costly. They are also subject to specific and sometimes intricate tax regulations. Professional management is often necessary to ensure proper administration and investment strategy.

The efficacy of irrevocable trusts as a wealth transfer strategy is evident in their widespread use among prominent families and individuals. The Rockefeller family's multi-generational wealth preservation through generation-skipping trusts serves as a prime example. Similarly, the Walton family (of Walmart) utilized Grantor Retained Annuity Trusts (GRATs), a specific type of irrevocable trust, to transfer significant portions of company shares to heirs with minimal tax consequences. Numerous high-net-worth individuals employ Charitable Remainder Trusts to support philanthropic endeavors while simultaneously benefiting heirs and mitigating taxes. These real-world examples underscore the power and flexibility of irrevocable trusts in achieving complex wealth management objectives.

When considering an irrevocable trust as part of your wealth transfer strategy, meticulous planning and professional guidance are essential. Working with an experienced estate planning attorney and a qualified tax advisor is paramount. Engaging a professional trustee with expertise in trust administration can ensure efficient management and adherence to regulations. Regularly reviewing trust investments and distributions is critical to maintain alignment with long-term financial goals. Ensuring the trust is adequately funded to meet its intended objectives is crucial, as is considering the impact of varying state trust laws.

Irrevocable trusts deserve their place in the wealth transfer strategy discussion due to their potent combination of tax benefits, asset protection, and generational wealth management capabilities. While the complexities necessitate careful planning and professional oversight, the potential rewards make them a compelling option for those seeking to secure their financial legacy.

2. Gifting Strategies

Gifting strategies are a powerful tool in wealth transfer planning, allowing you to proactively reduce your taxable estate while directly benefiting your loved ones. This approach involves transferring assets to beneficiaries during your lifetime, strategically utilizing annual gift tax exclusions and lifetime exemptions to minimize tax implications. By gifting assets now, you not only reduce the size of your estate, potentially saving your heirs significant estate taxes in the future, but you also gain the satisfaction of seeing how recipients manage the wealth you've worked hard to build. Furthermore, any appreciation of these gifted assets occurs outside of your estate, further amplifying the tax advantages.

One of the key features of gifting strategies is the annual gift tax exclusion, which allows you to gift up to $17,000 per recipient in 2023 (increasing to $18,000 in 2024) without incurring gift tax. This exclusion applies to each recipient, meaning a married couple can gift double that amount—$34,000 per recipient in 2023 ($36,000 in 2024)—without filing a gift tax return. Beyond the annual exclusion, you can also leverage the lifetime gift and estate tax exemption, a substantial amount currently set at $12.92 million per individual in 2023 ($13.61 million in 2024). This exemption allows you to gift considerable sums over your lifetime or at death without incurring federal gift or estate tax. Additionally, direct payments for medical and educational expenses are exempt from gift tax, providing another avenue for tax-efficient wealth transfer. Gifting can take various forms, including outright gifts of cash or assets, or gifts to trusts designed to protect and distribute assets according to your wishes. 529 plans offer a particularly attractive option for education funding, allowing for accelerated gifting equivalent to five years' worth of annual exclusions upfront ($85,000 per beneficiary in 2023).

Gifting strategies deserve a prominent place in any comprehensive wealth transfer plan due to their numerous advantages. They allow for proactive estate reduction, minimizing potential estate tax burdens for your heirs. The immediacy of gifting allows you to witness the impact of your generosity and potentially guide recipients in responsible wealth management. Gifting strategies can be tailored to specific needs, such as funding education through 529 plans or providing financial security through trusts. However, it’s crucial to acknowledge the potential drawbacks. Gifting is generally irrevocable, meaning you relinquish control over the gifted assets. While gifts may not be taxable, they may still require filing a gift tax return. Gifting also removes the opportunity for a step-up in basis, which would occur at death and could reduce capital gains taxes for your heirs. Finally, the current high exemption amounts are set to revert to pre-2018 levels in 2026, significantly reducing the amount that can be transferred tax-free.

The success of gifting strategies can be seen in the practices of prominent philanthropists. Warren Buffett, for example, has made substantial annual gifts of Berkshire Hathaway stock to his children's foundations. Bill and Melinda Gates employ a structured gifting program for their children while channeling the majority of their wealth towards philanthropic endeavors. These examples demonstrate the diverse ways gifting can be implemented to achieve specific financial and family goals.

Tips for Effective Gifting:

- Meticulous Record Keeping: Maintain detailed records of all gifts for tax purposes.

- Strategic Timing: Consider asset valuation fluctuations to maximize the value transferred.

- Financial Education: Couple gifting with financial education for recipients to promote responsible wealth management.

- Business Interests: Explore gifting non-voting shares to transfer value while retaining control of your business.

- Sunset Provision Awareness: Understand the implications of the scheduled reduction in lifetime exemptions in 2026 and plan accordingly.

By understanding the intricacies of gifting strategies and seeking professional guidance, you can create a tailored plan that aligns with your financial objectives and family values, ensuring a smooth and tax-efficient transfer of wealth to future generations.

3. Family Limited Partnerships (FLPs)

Family Limited Partnerships (FLPs) are a powerful wealth transfer strategy allowing families to move assets to the next generation while minimizing gift and estate taxes and maintaining a significant degree of control. An FLP is a legal entity structured with general partners (typically the parents) and limited partners (typically the children). This structure allows the senior generation to gradually transfer economic value to their heirs while retaining management control over the assets held within the partnership. The real power of the FLP lies in its ability to leverage valuation discounts, often between 20-40%, when gifting limited partnership interests. These discounts recognize the lack of marketability and control associated with limited partnership interests, effectively reducing the taxable value of the gift. This makes FLPs a highly effective tool for passing on significant wealth without incurring substantial tax burdens.

FLPs deserve a place on any list of wealth transfer strategies because of their unique combination of tax advantages and control features. They offer a structured approach to succession planning, facilitating the gradual transfer of wealth while educating younger generations about financial stewardship. The partnership can hold a variety of assets, including real estate, business interests, stocks, bonds, and other investments, making it a versatile tool for managing family wealth. The general partners maintain control over the assets within the FLP, making investment decisions and distributions. Limited partners benefit from the appreciation of the assets but have limited voting rights and management authority.

Features and Benefits:

- Partnership Structure: Clear delineation between general and limited partners.

- Control Retention: General partners (typically parents) retain management authority.

- Valuation Discounts: Reduced taxable value of gifts due to lack of marketability and minority interest discounts.

- Asset Diversification: FLPs can hold a wide range of assets.

- Liability Protection: Limited partners are shielded from personal liability for partnership debts.

- Succession Planning: Facilitates intergenerational wealth transfer and fosters financial education.

Pros:

- Enables wealth transfer while maintaining family control.

- Significant tax savings through valuation discounts.

- Consolidated asset management.

- Asset protection from creditors.

- Promotes financial stewardship among younger generations.

Cons:

- Complex establishment and maintenance.

- Potential IRS scrutiny.

- Requires a legitimate business purpose beyond tax savings.

- Ongoing administrative costs and requirements.

- Strict adherence to partnership formalities is crucial.

Examples of Successful Implementation:

- The Pritzker family (Hyatt Hotels) famously used FLPs to distribute hotel business interests to family members, minimizing estate taxes and facilitating a smooth succession plan.

- The Mars family (Mars candy company) has also utilized partnership structures for effective business succession.

- Many real estate families utilize FLPs to transfer property portfolios to the next generation with a significantly reduced tax impact.

Actionable Tips for Utilizing FLPs:

- Legitimate Business Purpose: Ensure the FLP has a demonstrable business purpose beyond tax minimization. Consult with experienced legal counsel to establish a valid purpose and structure.

- Separate Assets: Maintain strict separation between personal and partnership assets. Commingling funds can jeopardize the FLP's legal standing.

- Formal Meetings and Documentation: Hold regular partnership meetings with detailed minutes documenting all decisions and transactions.

- Income Distribution: Distribute income according to the partnership agreement and the respective ownership interests.

- Legal Counsel: Work with experienced attorneys specializing in FLPs and familiar with recent tax court cases to ensure compliance and minimize potential challenges.

By carefully considering the pros and cons and adhering to best practices, high-net-worth individuals can utilize FLPs as a valuable tool for wealth preservation and transfer, ensuring a smoother transition of assets to future generations.

4. Charitable Remainder Trusts (CRTs)

Charitable Remainder Trusts (CRTs) represent a sophisticated wealth transfer strategy that allows affluent individuals to achieve multiple financial and philanthropic goals simultaneously. As a key component of a comprehensive wealth transfer plan, CRTs offer significant tax advantages while ensuring a steady income stream for beneficiaries and ultimately supporting chosen charities. This strategy deserves its place on this list because it effectively blends tax efficiency, income generation, and charitable giving.

How CRTs Work:

A CRT is an irrevocable trust agreement where you transfer assets (cash, securities, real estate) into the trust. The trust then pays income to designated beneficiaries (yourself, family members, or others) for a specified term (up to 20 years) or for the lifetimes of the beneficiaries. After this period, the remaining assets in the trust are distributed to the pre-selected charitable organization(s).

There are two primary types of CRTs:

- Charitable Remainder Annuity Trust (CRAT): Pays a fixed annual amount to the beneficiaries. The annual payment is determined at the creation of the trust and remains constant throughout its term.

- Charitable Remainder Unitrust (CRUT): Pays a variable annual amount to the beneficiaries, typically a fixed percentage of the trust's annually revalued assets. This can provide inflation protection and potential for higher payouts if the trust assets appreciate.

Benefits and Features:

- Income Stream: Provides a reliable income stream for you or your designated beneficiaries.

- Tax Advantages: Offers several substantial tax benefits, including an immediate income tax deduction for the present value of the charitable remainder, avoidance of capital gains tax on appreciated assets transferred to the trust, and a reduction in the taxable estate.

- Philanthropic Impact: Enables you to support your chosen charities while also benefiting yourself and your heirs.

- Asset Diversification: Allows for the sale of appreciated assets within the trust without incurring immediate capital gains tax, facilitating diversification of investments without tax consequences.

Pros and Cons:

Pros:

- Immediate income tax charitable deduction

- Avoidance of capital gains tax on appreciated assets donated to the trust

- Reduction of taxable estate

- Income stream for donor or other beneficiaries

- Fulfillment of philanthropic goals

Cons:

- Irrevocable – cannot be changed once established

- Complex to set up and administer, requiring professional guidance

- Charitable component must be at least 10% of the initial fair market value

- Subject to private foundation rules in some cases

- Income payments are taxable to recipients

Examples of Successful Implementation:

- Media mogul Ted Turner famously donated $1 billion of Time Warner stock to a charitable trust, securing significant tax benefits while supporting the United Nations Foundation.

- Actor Paul Newman utilized charitable trusts as part of his comprehensive estate plan, ultimately leading to all profits from Newman's Own, Inc. going to charity.

- Many university donors establish CRTs to fund scholarships while simultaneously receiving lifetime income.

Actionable Tips for Wealth Transfer Using CRTs:

- Maximize Tax Benefits: Consider using a CRUT during high-income years to maximize the value of the income tax deduction.

- Capital Gains Tax Savings: Fund the CRT with highly appreciated assets to maximize capital gains tax savings.

- Benefit Heirs: Use CRTs in conjunction with wealth replacement life insurance to ensure that heirs are not disadvantaged by the charitable donation.

- Illiquid Assets: A "flip" CRUT can be a useful strategy for illiquid assets that are expected to appreciate significantly and will eventually be sold.

- Choose Wisely: Carefully select reputable charitable organizations with long-term financial sustainability to ensure your philanthropic goals are realized.

When and Why to Use CRTs:

CRTs are a powerful wealth transfer strategy for individuals seeking to:

- Reduce their current and future tax burden

- Generate a reliable income stream for themselves or others

- Make a significant charitable contribution

- Simplify estate planning and minimize estate taxes

By carefully structuring a CRT with the help of experienced legal and financial professionals, wealthy individuals can optimize their wealth transfer strategy, achieving both personal financial goals and philanthropic objectives. This method offers a unique blend of tax efficiency, income generation, and charitable giving, solidifying its importance as a wealth transfer strategy.

5. Grantor Retained Annuity Trusts (GRATs)

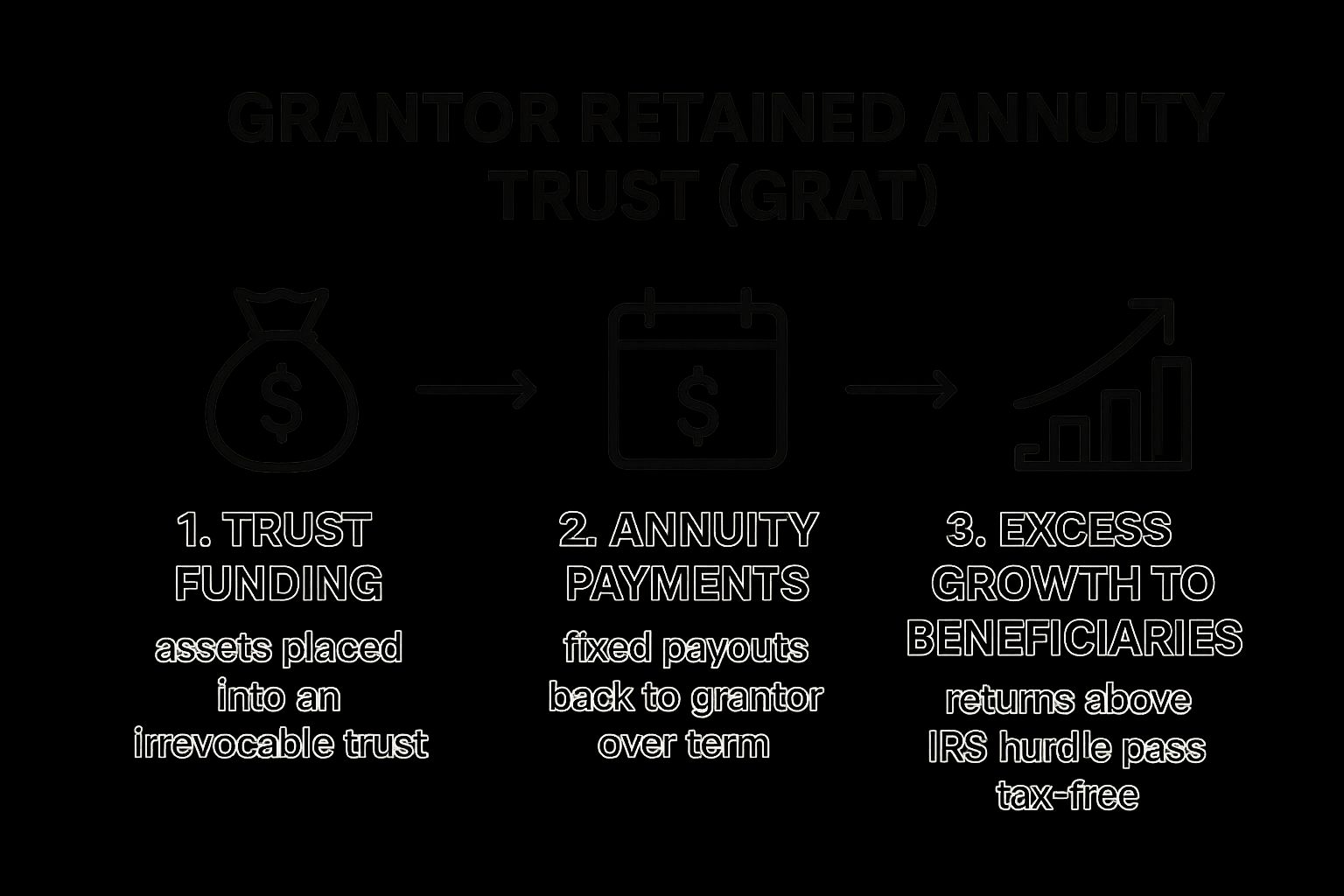

Grantor Retained Annuity Trusts (GRATs) are sophisticated estate planning tools that facilitate the transfer of appreciating assets to beneficiaries while minimizing gift tax liabilities. This strategy allows individuals to essentially "freeze" the value of assets for gift tax purposes, passing any future appreciation to heirs tax-free. A GRAT involves placing assets into an irrevocable trust for a predetermined period (typically 2-10 years). During this term, the grantor receives fixed annuity payments. Crucially, the gift tax is calculated based on the present value of the assets transferred, less the present value of the annuity payments. If the assets appreciate faster than the IRS-mandated interest rate (Section 7520 rate), the excess growth passes to the beneficiaries without incurring gift tax at the end of the trust term. This makes GRATs a powerful wealth transfer strategy, particularly in low-interest-rate environments.

The infographic illustrates the process flow of a GRAT, outlining the key steps involved. First, the grantor funds the GRAT with assets. Then, over the GRAT term, the grantor receives predetermined annuity payments. Finally, at the end of the term, the remaining assets, including any appreciation exceeding the 7520 rate, transfer to the beneficiaries. This visualization emphasizes the timing and movement of assets within a GRAT, highlighting how appreciation bypasses gift tax.

GRATs deserve a place on any list of wealth transfer strategies due to their potential for significant tax savings. Key features include fixed annuity payments for the grantor, a design aimed at minimizing or eliminating gift tax ("zeroed-out GRAT"), and particular effectiveness with high-growth or volatile assets. These trusts can be structured in series ("rolling GRATs") for ongoing benefits, maximizing wealth transfer over time. They are most effective when interest rates are low, creating a larger spread between asset growth and the IRS hurdle rate.

Pros:

- Transfers asset appreciation above the IRS hurdle rate tax-free to beneficiaries.

- Minimal or no gift tax cost when structured correctly.

- Return of original principal to the grantor through annuity payments.

- Highly effective for pre-IPO stock or other high-growth assets.

- Grantor retains control of the assets during the trust term.

Cons:

- Mortality risk: If the grantor dies during the trust term, assets may be included in the estate.

- Limited effectiveness in high-interest rate environments.

- Requires assets to outperform the IRS Section 7520 rate to be beneficial.

- Administrative complexity and associated costs.

- Political risk: GRATs have been targeted for potential legislative changes.

Examples of Successful Implementation:

- Mark Zuckerberg reportedly used GRATs before Facebook's IPO to transfer shares with minimal tax implications.

- The Walton family has extensively used GRATs to transfer Walmart shares to heirs.

- Sheldon Adelson transferred billions in Las Vegas Sands stock to family members using rolling GRATs.

Tips for Utilizing GRATs:

- Consider short-term GRATs (2-3 years) to minimize mortality risk.

- Fund GRATs with volatile assets that have significant upside potential.

- Structure as a "rolling GRAT" where annuity payments fund new GRATs, creating a continuous wealth transfer process.

- Time the creation of a GRAT to coincide with temporarily depressed asset values.

- Consider pairing a GRAT with an Intentionally Defective Grantor Trust (IDGT) for the remaining assets after the GRAT term.

Key Figures and Institutions:

- Richard Covey: Developed the modern zeroed-out GRAT technique.

- Carlyn McCaffrey: Estate planning attorney who pioneered advanced GRAT strategies.

- Goldman Sachs' Private Wealth Management group: Popularized GRATs among executives.

GRATs are complex instruments. Consulting with experienced estate planning professionals is essential to determine their suitability for your individual circumstances and to ensure proper structuring and implementation as part of a comprehensive wealth transfer strategy.

6. Qualified Personal Residence Trusts (QPRTs)

As part of a comprehensive wealth transfer strategy, Qualified Personal Residence Trusts (QPRTs) offer a unique approach to passing on significant residential property to heirs while minimizing gift and estate tax liabilities. This method allows you to transfer your primary residence or a vacation home to your beneficiaries at a reduced gift tax value, effectively freezing the asset's value for tax purposes and removing future appreciation from your taxable estate.

How QPRTs Work:

You establish an irrevocable trust and transfer ownership of your residence to it. You specify a term length (typically 5-15 years) during which you retain the right to live in the property. The gift tax value is calculated based on the present value of the future interest your beneficiaries will receive, discounted based on the length of the retained term and prevailing IRS interest rates. After the term expires, ownership transfers to the beneficiaries, and the property's subsequent appreciation is no longer part of your taxable estate. You can then rent the property back from the trust at fair market value.

Why QPRTs Deserve a Place in Your Wealth Transfer Strategy:

For individuals with significant wealth tied up in real estate, especially property expected to appreciate considerably, a QPRT can be a powerful tool. It offers a way to strategically remove a valuable asset from your estate while still enjoying its use. This is particularly beneficial in high-growth real estate markets.

Features and Benefits:

- Reduced Gift Tax: The discounted gift tax value allows you to leverage your lifetime gift tax exemption more effectively.

- Estate Tax Savings: Future appreciation of the property is excluded from your estate.

- Continued Use: You maintain the right to live in the property for the specified term.

- Ideal for Appreciating Assets: Maximizes tax benefits for properties expected to increase in value.

- Preserves Family Homes: Facilitates the transfer of emotionally significant properties to future generations.

Pros:

- Transfers residence at a discounted gift tax value.

- Removes future appreciation from the taxable estate.

- Allows continued use of the property during the trust term.

- Particularly effective for properties likely to appreciate significantly.

Cons:

- Mortality Risk: If the grantor dies during the term, the property returns to the taxable estate.

- Loss of Step-Up in Basis: Beneficiaries don't receive a step-up in basis at the grantor's death.

- Must Outlive Trust Term: Benefits are only realized if the grantor survives the term.

- Rent Payments After Term: Fair market rent must be paid to the trust to continue living in the property.

- Less Effective in High Interest Rate Environments: The discount is reduced when interest rates are high.

Examples of Successful Implementation:

- Jacqueline Kennedy Onassis utilized a QPRT for her Martha's Vineyard estate.

- Many Silicon Valley executives use QPRTs for high-value California properties.

- Family vacation homes in desirable locations are frequently transferred via QPRTs.

Actionable Tips:

- Consider Age and Health: Factor in the grantor's life expectancy when determining the term length.

- Balance Term Length and Risk: Longer terms offer greater tax savings but increase mortality risk.

- Low Interest Rate Advantage: QPRTs are most effective when interest rates are low.

- Plan for Rent Payments: Have a strategy for paying fair market rent after the term ends.

- Consider Alternative Housing: Explore purchasing a new residence with proceeds from other assets if rent payments are undesirable.

When and Why to Use a QPRT:

A QPRT is a valuable wealth transfer strategy when:

- You own a primary residence or vacation home expected to appreciate significantly.

- You want to minimize estate and gift taxes.

- You want to maintain use of the property for a defined period.

- You want to transfer ownership to your heirs in a tax-advantaged manner.

While a QPRT offers significant advantages, it's crucial to carefully consider the potential drawbacks and consult with experienced estate planning professionals to determine if it's the right strategy for your specific circumstances. The complexity of QPRTs necessitates professional guidance to ensure proper structuring and compliance with IRS regulations.

Wealth Transfer Strategies Comparison

| Strategy | Implementation Complexity 🔄 | Resource Requirements 💡 | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Irrevocable Trusts | High – complex legal & tax setup | High – professional legal & trustee | Significant estate tax reduction, asset protection | Multi-generational wealth transfer, asset protection | Strong estate tax reduction, creditor protection, controlled wealth distribution |

| Gifting Strategies | Moderate – straightforward gifts | Low to Moderate – record keeping, tax filing | Immediate wealth transfer, reduced taxable estate | Routine wealth transfer, education funding, philanthropy | Immediate benefit to heirs, annual tax-efficient transfers, direct guidance possible |

| Family Limited Partnerships | High – complex partnership setup | High – legal, tax, and administration | Wealth transfer with valuation discounts, asset consolidation | Family business succession, real estate portfolios | Maintains family control, tax savings via discounts, creditor protection |

| Charitable Remainder Trusts | High – specialized legal setup | High – legal, tax, and trustee fees | Income stream + charitable deduction + estate tax reduction | Philanthropy combined with income planning | Income tax deduction, capital gains tax avoidance, philanthropic impact |

| Grantor Retained Annuity Trusts (GRATs) | High – detailed structuring and monitoring | Moderate to High – administration & tax advice | Transfer asset appreciation tax-free if outperform hurdle | High-growth assets, volatile holdings, concentrated stock positions | Minimal gift tax, transfers appreciation, retains control during term |

| Qualified Personal Residence Trusts (QPRTs) | Moderate to High – legal setup and term planning | Moderate – legal and ongoing planning | Transfers residence at discounted gift tax value | Personal residences likely to appreciate, emotional family homes | Retain property use, remove future appreciation from estate, discounted gift value |

Planning for a Secure Future: Putting Wealth Transfer Strategies into Action

Effectively transferring wealth involves more than simply distributing assets; it requires a strategic approach that minimizes tax implications, protects your legacy, and provides for your loved ones according to your wishes. This article has explored several key wealth transfer strategies, including irrevocable trusts, gifting strategies, family limited partnerships (FLPs), charitable remainder trusts (CRTs), grantor retained annuity trusts (GRATs), and qualified personal residence trusts (QPRTs). Each of these tools offers unique benefits and considerations, making it crucial to understand their nuances and how they can work together as part of a comprehensive plan.

Mastering these wealth transfer strategies empowers you to take control of your financial future and ensure the smooth transition of your assets. By minimizing estate taxes and other potential liabilities, you can maximize the value passed on to your heirs and charitable causes. The benefits extend beyond simple monetary value, offering peace of mind knowing your wealth is structured to support future generations and achieve your philanthropic goals.

Taking the next steps is crucial. Begin by carefully reviewing your current financial situation and long-term objectives. Which of the wealth transfer strategies discussed resonates most with your circumstances? Consider the level of control you wish to retain, your charitable giving goals, and the complexity of your assets. To ensure the smooth transfer of your wealth and secure your family's future, consider consulting with expert estate planners. They can guide you through the process of creating wills, establishing trusts, and implementing other asset protection strategies. Resources like the article on expert estate planning for families from America First Financial can provide valuable insights into this process. Seeking professional guidance from a financial advisor specializing in wealth transfer strategies is highly recommended. They can help you develop a tailored plan that aligns with your unique needs and maximizes the impact of your legacy.

Ultimately, proactive planning is the cornerstone of successful wealth transfer. By taking action today and implementing the strategies outlined here, you are not simply transferring assets—you are securing a legacy for generations to come.